Kenya's Electric Mobility Policy Faces Its First Fiscal Test

Roam Electrical and mechanical engineers building a Roam Air motorcycle

Kenya’s National Electric Mobility policy was launched in February 2026 by the Ministry of Roads and Transport, marking an important milestone in the country’s transition toward electric mobility. The policy signalled the government’s commitment to creating an enabling policy and regulatory environment for the widespread adoption of electric vehicles (“EVs”). Central to that commitment were the tax incentives introduced under the Finance Act 2025, which the policy identified as a key mechanism for accelerating investment and adoption.

Yet only two months later, the Treasury tabled a Finance Bill that would have reversed one of those flagship incentives. Parliament ultimately rejected the proposal, but the episode exposed how quickly fiscal policy can undermine broader policy objectives. It also highlighted a wider lesson: for emerging industries, policy certainty can be just as important as policy ambition.

Image 1: The Differences between Zero-Rated and Exempt Mechanisms

The proposed change was easy to overlook because it did not introduce a new tax. Instead, it involved a technical change to the way VAT was applied.

At first glance, the Finance Bill 2026 seemed to pay little attention towards green technologies. It proposed no new tax on electric buses or solar batteries. Instead, it reclassified several goods from zero-rated to VAT-exempt. Although the distinction appeared technical, it would have had significant commercial consequences. Much of the public discussion therefore, reduced the proposal to a "16% VAT increase", overlooking the mechanics that would actually have increased costs.

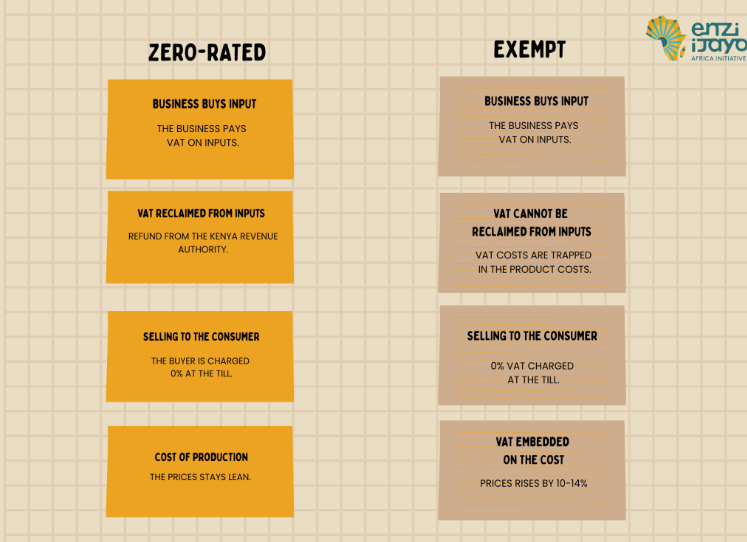

Under a zero-rated system, businesses selling EVs or lithium-ion batteries charge customers no VAT while still recovering the VAT paid on imported components, transport and other inputs. This keeps production and assembly costs relatively low.

VAT exemption works differently. Businesses still do not charge VAT to customers, but they lose the ability to recover VAT paid throughout their supply chains. Those unrecoverable costs are typically passed on through higher prices. Industry estimates suggested that the proposed change would have increased retail prices by between 10% and 14%, embedding those additional costs into every electric bus, motorcycle and battery sold.

Kenya's electric mobility industry remains heavily dependent on imported inputs. Although vehicle assembly is increasingly taking place locally, critical components such as lithium-ion battery cells are still manufactured abroad. For that reason, the proposed shift from zero-rating to VAT exemption would have been far more than a technical tax adjustment. It would have increased production costs across the value chain, weakening the competitiveness of an industry that the government had spent only months promoting through its new electric mobility policy.

The Sequence of Events:

The timeline illustrates how close Kenya came to enacting legislation that would have undermined the very incentives it had only recently introduced.

February 3, 2026, the National Electric Mobility Policy was launched. The policy identified the zero-rating provisions introduced under the Finance Act 2025 as a cornerstone incentive and reaffirmed the government's commitment to expanding fiscal support for the sector.

April 2026, the Treasury Cabinet Secretary announced plans to cancel an order for 2,500 petrol and diesel vehicles in favour of purchasing 3,000 locally assembled EVs. The announcement reinforced the government's public commitment to electric mobility, even as the Finance Bill was preparing to withdraw one of the sector's principal incentives.

April 30, 2026, the National Treasury Cabinet Secretary presented the Finance Bill, 2026 (the Bill) to Parliament, part of which includes the proposed VAT changes to broaden the tax base and increase domestic revenue collection, arguing that removing zero-rated status from selected goods would reduce VAT refund obligations, improve tax efficiency, and help finance the government's growing expenditure and fiscal consolidation targets.

May 2026, a public participation window, mandated by the constitution, was opened for the proposed reclassification, which attracted sustained opposition. The Institute of Certified Public Accountants of Kenya raised concerns that the green economy was not ready and was too immature to absorb the additional costs. The Law Society of Kenya also flagged that the burden would ultimately fall on consumers. The submissions consistently highlighted a broader concern arguing that the proposal was inconsistent with the government's own electric mobility policy.

June 2026, having considered the submissions, the Departmental Committee on Finance and National Planning (the “Committee”) recommended dropping the reclassifications and maintaining the zero-rating in response to the objections raised.

June 18, 2026, the National Assembly adopted the Committee’s recommendations and passed the Finance Bill with zero-rating provisions maintained.

June 23, 2026, President Ruto assented to the Bill, enacting the Finance Act of 2026.

1 July 2026, the Act came into force, with the zero-rating for solar and electric mobility products continuing uninterrupted.

Beyond This Budget Cycle:

The Finance Bill 2026 demonstrates that Kenya’s legislative and public participation processes can work as intended. Industry stakeholders identified a technically significant issue, Parliament scrutinised the proposal, and legislators ultimately chose to preserve a key incentive supporting a nascent electric mobility industry despite the government’s need to raise additional revenue.

The episode also exposes a broader challenge. Although Parliament ultimately preserved the zero-rating provisions, nothing prevents a similar proposal from reappearing in future Finance Bills. For investors making long-term decisions, recurring uncertainty over fiscal incentives can be almost as damaging as their removal. Stable tax policy is therefore not simply a fiscal issue; it is an essential part of building confidence in Kenya's electric mobility transition. It also highlights the need to better align fiscal policy with industrial policy, ensuring that fiscal measures support, rather than undermine, the government’s broader industrial objectives.

Subscribe to our newsletter below and stay informed on the latest updates, engagements, and news!